Preparing for the 2026 Global Insurance Symposium in Des Moines: What Insurance Leaders Should Be Thinking About

As insurance leaders prepare to gather in Des Moines, Iowa, for the Global Insurance Symposium, the context surrounding this year’s event feels especially consequential. The global insurance industry is facing a convergence of pressures that are no longer theoretical or distant — they are operational, financial, and increasingly societal in nature. From climate-driven catastrophe exposure and affordability challenges to rapid advances in data, artificial intelligence, and automation, insurers are being asked to rethink long-standing assumptions about risk, pricing, and responsibility. For many leaders, the Global Insurance Symposium offers a rare opportunity to step back from day-to-day execution and reflect on whether their organizations are equipped to withstand and adapt to the forces reshaping insurance markets.

Climate Risk and the Future of Property & Casualty Insurance

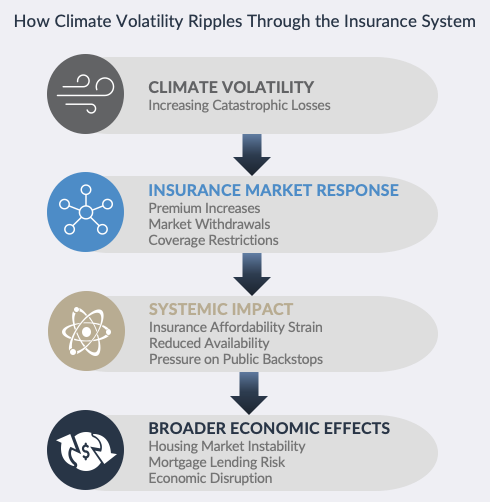

One of the most pressing themes shaping the insurance landscape today is climate risk, not as a distant or abstract concern, but as a force actively reshaping property and casualty(P&C) insurance markets in real time.

Across regions, insurers are grappling with increasing exposure to natural perils such as hurricanes, wildfires, and floods. Losses are rising in both frequency and severity, and in many cases, they are occurring across multiple regions simultaneously.

In response, insurers have taken difficult but rational actions:

- Exiting certain markets altogether

- Raising premiums and deductibles

- Reducing coverage limits or modifying policy terms

The cumulative effect has been growing affordability and availability challenges for policyholders. In some areas, insurance is becoming difficult to obtain at a price that homeowners and businesses can reasonably sustain, creating ripple effects for housing markets, mortgage lending, and local economies.

These trends raise fundamental questions about the durability of traditional operating and risk-transfer models. Geographic diversification and reinsurance remain critical tools, but they are increasingly strained in an environment where climate impacts are more correlated across regions and even across continents.

Climate risk is also testing the boundary between private insurance markets and public responsibility. In certain cases, societies have chosen to backstop risks through public programs, such as flood insurance. Yet these programs face their own sustainability challenges as loss experience intensifies and funding gaps widen.

Over the long term, meaningful risk mitigation will require coordinated action beyond the insurance sector. Urban and land-use planning, strengthened building codes and construction standards, and sustained infrastructure investment focused on resilience rather than recovery will all play a critical role in stabilizing risk.

For insurance leaders, the implication is clear: climate risk can no longer be treated solely as a technical underwriting or pricing problem. It is a systemic issue that will shape product design, capital strategy, and market participation for years to come.

Reinsurance, Capital Markets, and Risk Distribution

Reinsurance has long been central to insurance risk management and capital efficiency. However, as climate-driven losses intensify, its role is becoming even more strategic.

The question for insurers is no longer whether to use reinsurance, but how to structure and integrate it effectively as catastrophe exposure grows and risk correlation increases. Traditional reinsurance, particularly access to international capacity, remains critical, but it is no longer the only mechanism available.

Increasingly, insurers are turning to capital markets to diversify catastrophe risk. Insurance-linked securities (ILS), including catastrophe bonds, provide an additional avenue for transferring risk beyond traditional reinsurance markets. By tapping into broader global capital pools, insurers can expand risk-bearing capacity and improve portfolio resilience.

For insurance leaders, reinsurance strategy now directly influences underwriting capacity, pricing flexibility, and decisions about which markets remain viable. As climate pressures grow, the structure of reinsurance programs will play a defining role in long-term operational sustainability.

Data, Artificial Intelligence, and the Changing Nature of Risk

Beyond climate and capital dynamics, advances in data analytics, artificial intelligence (AI), and machine learning are reshaping underwriting and pricing across the insurance industry.

This shift has significant economic implications. Improved data narrows long-standing information gaps between insurers and policyholders, reducing adverse selection and moral hazard. As pricing becomes more closely aligned with individual risk, insurers may improve sustainability in historically challenging lines — including long-term care — where uncertainty around future loss experience has driven volatility.

However, greater precision also raises important questions around fairness and equity. Certain data signals may function as proxies for protected characteristics, even if they are not explicitly included in pricing models. As insurers rely more heavily on AI-driven underwriting, expectations for transparency, explainability, and responsible use continue to rise.

Technological innovation is also redefining risk ownership itself. Autonomous vehicles, for example, blur traditional lines between driver responsibility and manufacturer liability, illustrating how advances in technology can reshape accountability across the insurance ecosystem.

These developments signal that technology is not simply enhancing existing models: it’s changing how risk is measured, priced, governed, and assigned.

Turning Insight into Strategic Direction

Taken together, climate volatility, evolving reinsurance markets, and rapid technological advancement illustrate a consistent reality for the insurance industry: the external environment is constantly evolving —and the pace of change is accelerating.

What distinguishes leading insurance organizations is not simply awareness of these forces, but the ability to convert insight into disciplined strategic direction.

As executives gather in Des Moines for the Global Insurance Symposium, a valuable exercise is to examine how their organizations are responding to the shifts already underway, starting with a few essential strategic planning questions:

- How clearly have we defined our long-term strategy, and is it consistently understood across leadership and business units?

- Where are the external pressures creating tension with our current business model?

- Do our current investments and priorities reflect the strategic direction we have set?

- How resilient is our organization under multiple plausible future scenarios?

These questions often reveal whether strategy is functioning as an active guide for decision-making or remaining disconnected from day-to-day realities.

In an environment defined by uncertainty, risk trade-offs, and rising societal expectations, insurance leaders who treat strategy as a disciplined process for setting direction, prioritizing action, and aligning the organization over time will be better positioned to adapt and sustain performance.

Sign UP to receive related Insights

Related Case STudies

View case studies

Trending Topics

View All

Schedule Your Session Today

Enter your information below and our team will contact you.